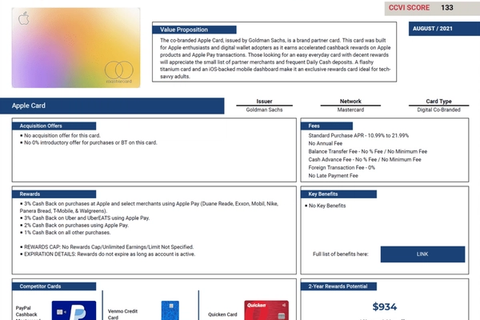

Bilt’s redesigned credit card lineup marks a clear break from its Wells Fargo–issued predecessor. The new structure introduces three distinct products, Blue, Obsidian, and Palladium, each aimed at a different consumer segment. From a value perspective, the reset is real. From an issuer perspective, the risks have been reduced, but not removed.

Using Panoramic Research’s Credit Card Value Index (CCVI), we assessed whether Bilt’s new cards truly deliver value, how they compare to competitive benchmarks, and whether the economics can work long term.

The Three Bilt Cards, Explained

Bilt Blue Card (No Annual Fee)

Positioning: Entry-level card tied to housing and everyday spend

Bilt Blue is designed to bring renters into the Bilt ecosystem without an annual fee. It earns rewards connected to rent and select everyday categories, with value maximized through Bilt point redemptions rather than simple cash back.

CCVI score: 291

Why it matters: This score places Bilt Blue far above traditional no-fee cash-back cards. The value is real, but it depends on engagement. Passive users may not fully realize it.

Bilt Obsidian Card ($95 annual fee)

Positioning: Mid-tier lifestyle and rewards card

Obsidian targets consumers willing to pay a modest fee for better earn rates and benefits. It competes in a crowded $95 segment but differentiates itself through Bilt’s transfer partners and experiential rewards.

CCVI score: 302

Why it matters: Obsidian outperforms most mid-tier competitors on a value-adjusted basis, though it asks more of the consumer in terms of understanding how to redeem points effectively.

Bilt Palladium Card ($495 annual fee)

Positioning: Premium lifestyle and travel-adjacent card

Palladium brings premium benefits and credits into the Bilt ecosystem. It is aimed at high-spend, highly engaged users who are already active in rewards programs.

CCVI score: 405

Why it matters: Palladium is a legitimate premium product, but it competes with best-in-class travel cards that offer simpler and more established value propositions.

How Bilt Compares on Value (CCVI Benchmarks)

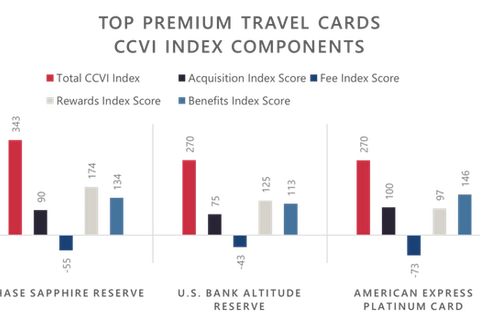

Premium Tier

| Card | CCVI Score |

|---|---|

| Bilt Palladium | 405 |

| Amex Platinum | 459 |

| Chase Sapphire Reserve | 444 |

| Citi Strata Elite | 298 |

| Capital One Venture X | 292 |

Panoramic view: Palladium holds its own against premium competitors, but still trails the two most established travel cards, largely due to clarity and ease of value realization.

Mid-Tier ($95 Annual Fee)

| Card | CCVI Score |

|---|---|

| Blit Obsidian | 302 |

| Chase Sapphire Preferred | 253 |

| Amex Gold | 212 |

| Capital One Venture | 212 |

| Citi Strata Premier | 199 |

| U.S. Bank Shopper Cash | 184 |

Panoramic view: Obsidian leads this group on CCVI, reflecting benefits density rather than simplicity. Cards with lower scores are often easier to understand.

No Annual Fee

| Card | CCVI Score |

|---|---|

| Bilt Blue | 291 |

| U.S. Bank Altitude Connect | 176 |

| Chase Freedom Unlimited | 173 |

| Citi Strata Card | 164 |

| Citi Double Cash | 162 |

| Capital One Savor Rewards | 155 |

| Discover it Cash Back | 153 |

| Amex Blue Cash Everyday | 148 |

| Wells Fargo Autograph | 133 |

Panoramic view: Bilt Blue is a structural outlier. Its score reflects ecosystem value, not just earn rates. That makes it compelling, and risky.

Understanding Redemption: Cash Back vs. Bilt Points

A key design choice in the new Bilt cards is the use of two parallel reward buckets: Bilt Points and cash back (Bilt Cash), a structure that adds flexibility but also increases complexity for consumers. While flexibility can be a strength, this structure creates real friction for many consumers.

Bilt Points: Where the Upside Lives

Bilt Points are the program’s primary value engine. They can be transferred to airline and hotel partners, used for travel, experiences, or applied in ways that often exceed one cent per point in value.

For engaged users, this is where Bilt’s CCVI advantage shows up. The strongest CCVI scores across the lineup assume that cardholders actively redeem points through high-value channels, not as statement credits.

Cash Back (Bilt Cash): Simplicity With a Trade-Off

Bilt Cash offers a simpler option. Rewards can be redeemed as cash or statement credits, removing the need to understand transfer partners or redemption mechanics.

The trade-off is value. Cash back redemptions generally deliver lower effective value than optimized point redemptions. In CCVI terms, cash back functions as a safety net rather than the primary source of value.

Why Two Buckets Create Confusion

From a consumer perspective, the dual-currency system raises practical questions: - Which rewards am I earning right now? - Which bucket should I redeem from first? - Am I leaving value on the table by choosing cash back?

For mainstream users, this added cognitive load can dilute perceived value. Consumers accustomed to single-currency cash-back cards may find the structure unintuitive.

The two-bucket system benefits sophisticated users who want flexibility. It also allows Bilt to appeal to a broader audience without forcing every cardholder into points-based redemptions.

However, CCVI analysis suggests a clear trade-off: the cards score highly on potential value, but that value is harder to realize. Without continued education and simplification, redemption confusion could become a drag on satisfaction and long-term engagement.

Are the New Bilt Cards Worth It?

From a value standpoint, yes, especially compared to the original Wells Fargo-issued Bilt card, which scored just 110 on CCVI. The redesigned lineup delivers materially higher potential value across all tiers.

That value, however, is not automatic. Consumers who default to cash back may under-realize the cards’ potential, while those willing to engage with Bilt Points stand to gain the most.

The 10% Intro APR: Signal or Substance?

One element of the new Bilt cards that stands out in the current market is the 10% introductory APR offered for the first year. On its face, this appears consumer-friendly, but in context it is less generous than it initially seems.

Most competitive cards with promotional financing offer 0% intro APRs on purchases, balance transfers, or both. Within Panoramic Research’s CCVI database, 118 of 342 cards currently include a 0% introductory rate. Against that backdrop, a 10% intro APR is unusual, but not market-leading.

The timing also matters. The offer arrives amid increased political attention on credit card interest rates, including proposals to cap APRs at lower levels. While it is difficult to assign intent, the structure of Bilt’s offer feels as much like signaling as it does a true value add.

For consumers who carry balances, 10% is meaningfully better than standard purchase APRs. For consumers accustomed to 0% offers, the benefit may feel underwhelming. From an issuer perspective, the offer helps limit interest income volatility without fully sacrificing revenue.

Issuer Risk: The Break-Even Challenge Remains

The Wells Fargo partnership struggled because reward costs tied to rent outpaced revenue. While Bilt’s new structure improves the math, the underlying challenge persists.

Key constraints: - Housing payments generate low interchange - Rewards costs scale predictably with rent volume

Offsets required for sustainability: - Non-housing discretionary spend - Annual fee revenue from Obsidian and Palladium - Breakage or delayed redemption of Bilt points - Interest income, despite competitive APR positioning

The most engaged users are also the most expensive users. If growth skews heavily toward rewards-savvy power users, profitability becomes harder to achieve.

Bilt’s leadership has signaled flexibility and willingness to adjust. That helps. Long-term success will depend on disciplined acquisition and continued simplification.

Final Panoramic Take

Bilt’s new cards represent a credible second act. CCVI data confirms a real improvement in value and competitiveness versus the original card. The lineup is differentiated and ambitious.

The open question is sustainability. These cards work best for engaged users and require careful economic management. For Bilt and its issuer, execution, not demand, will determine whether this program endures.